News

Seasonality of cryptoasset returns

Tick tock, next block. Bitcoin works like clockwork, as they say. Roughly every 10 minutes, a new block of transactions is timestamped into the public ledger.

Of course, time plays an important role in the Bitcoin protocol. But what about seasons?

Traditional financial research provides ample evidence of seasonality in stock returns. You’ve probably heard of the “January effect” or “Turnaround Tuesday.”

You read Long and Short Cryptocurrenciesour weekly newsletter containing information, news and analysis aimed at the professional investor. register here to receive it in your mailbox every Wednesday.

Statistically significant seasonal performance patterns can be observed over almost any time period: quarterly, monthly, weekly, daily, hourly, etc.

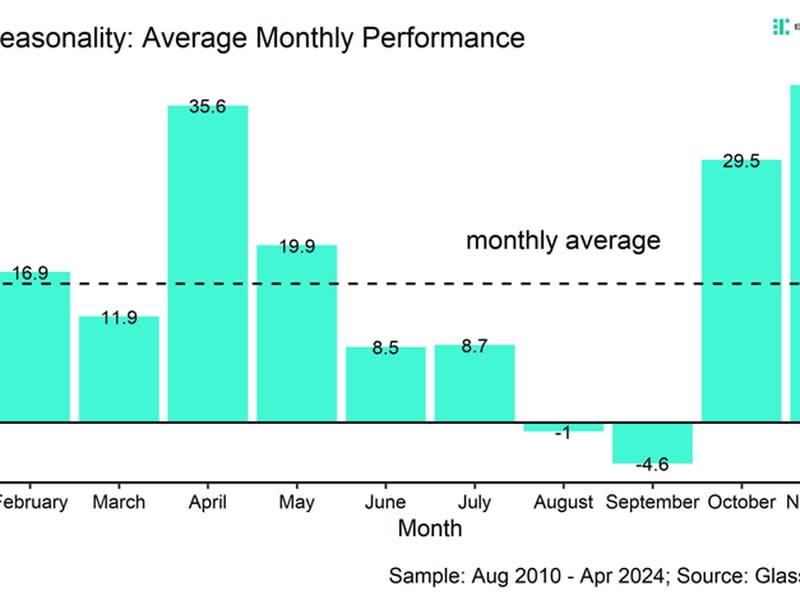

The adage “sell in May and walk away” has been around since the 19th century, as the summer months tend to show noticeably weak stock returns compared to other months of the year.

A look at Bitcoin’s average monthly returns reveals that the summer months between June and September also showed significantly lower than average returns.

Why should we care?

Well, if you had simply held cash during the months of August and September (when you were on vacation) and only invested in Bitcoin for the rest of the year, you would have outperformed a buy-and-hold Bitcoin investor by four times!

Therefore, statistically significant seasonal performance patterns could theoretically be used to derive meaningful alpha.

Additionally, the seasonal average performance model also suggests that Bitcoin could continue to rally over the next few weeks until around June, at which point the seasonal average performance model suggests that Bitcoin could take a breather over the summer months before continuing its climb towards the end of the year.

That being said, as mentioned above, seasonal performance patterns can be observed over almost any time period.

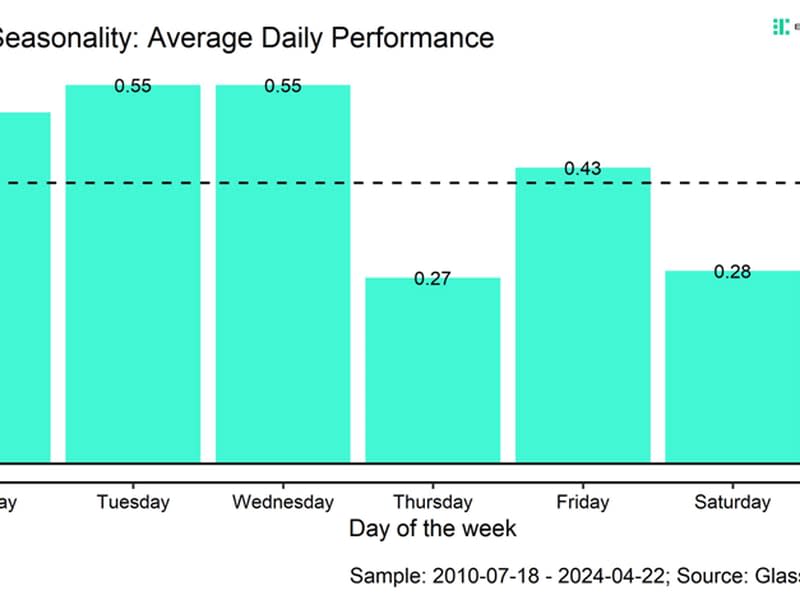

In this context, bitcoin appears to have performed best at the beginning of the week (Monday to Wednesday), while performance towards the end of the week and especially on the weekend has historically been below average.

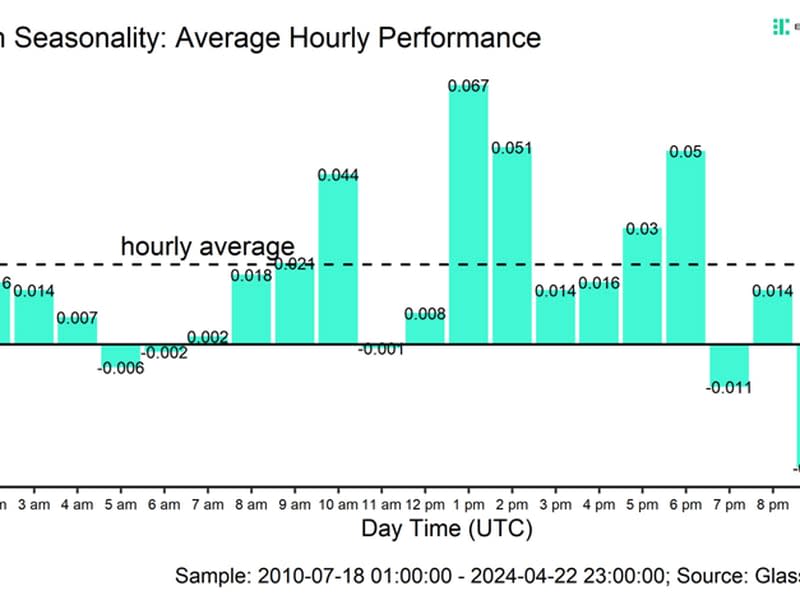

Similar trends can be observed across different trading hours: while performances during Asian trading hours (00:00 UTC – 06:00 UTC) were mostly below average, European (08:00 UTC – 16:30 UTC) and US (14:30 UTC – 21:00 UTC) trading hours typically show above average performances. That being said, towards the end of the US trading session (21:00 UTC), Bitcoin’s returns have historically been the worst.

The story continues

Similar intraday performance patterns can also be observed in the traditional forex market, where most trading volumes occur at the intersection between European and American trading hours (between 14:30 UTC and 16:30 UTC).

Bitcoin is traded 24/7/365 around the world, but price fluctuations are ultimately a product of human action. It’s no surprise, then, that the “sell in May and walk away” principle also seems to apply to Bitcoin’s return profile.

While Bitcoin continues to run like clockwork, its performance is ultimately determined by when we are awake or asleep, when we start work, and when most of us are on vacation or not at work.

Tick, tock, next block.

This is not investment advice.