News

How is blockchain changing financial services?

When Blythe Masters, a former JPMorgan Chase executive and one of Wall Street’s most prominent financiers, was named chief executive of blockchain company Digital Asset Holdings in 2015, many saw it as a sign that technology — to build secure transaction networks – would disrupt financial services.

At the time, Masters told Bloomberg News, “You should take this technology as seriously as you should have taken the development of the Internet in the early 1990s.”

Eight years later, blockchain startups, such as Digital Assets, have yet to make a big inroad into the world of finance beyond the realm of cryptocurrencies, where the technology originated. Masters left Digital Assets three years after joining. In May, she returned to Wall Street as part of the ill-fated effort to save Swiss bank Credit Suisse.

Crypto Crash Scares Industry

Following last year’s spectacular crypto booms, the question of how seriously the financial services industry should take blockchain seems even more up in the air than it was eight years ago. Late last year, following the collapse of cryptocurrency exchange FTX, several high-profile blockchain projects, including that of the Australian Stock Exchange, were put on hold.

Recommended

“A lot of the energy was going into the crypto aspect,” says Robert Ruark, who leads the U.S. fintech practice at Big Four accounting firm KPMG. “When the crash happened, all those investments went backwards.”

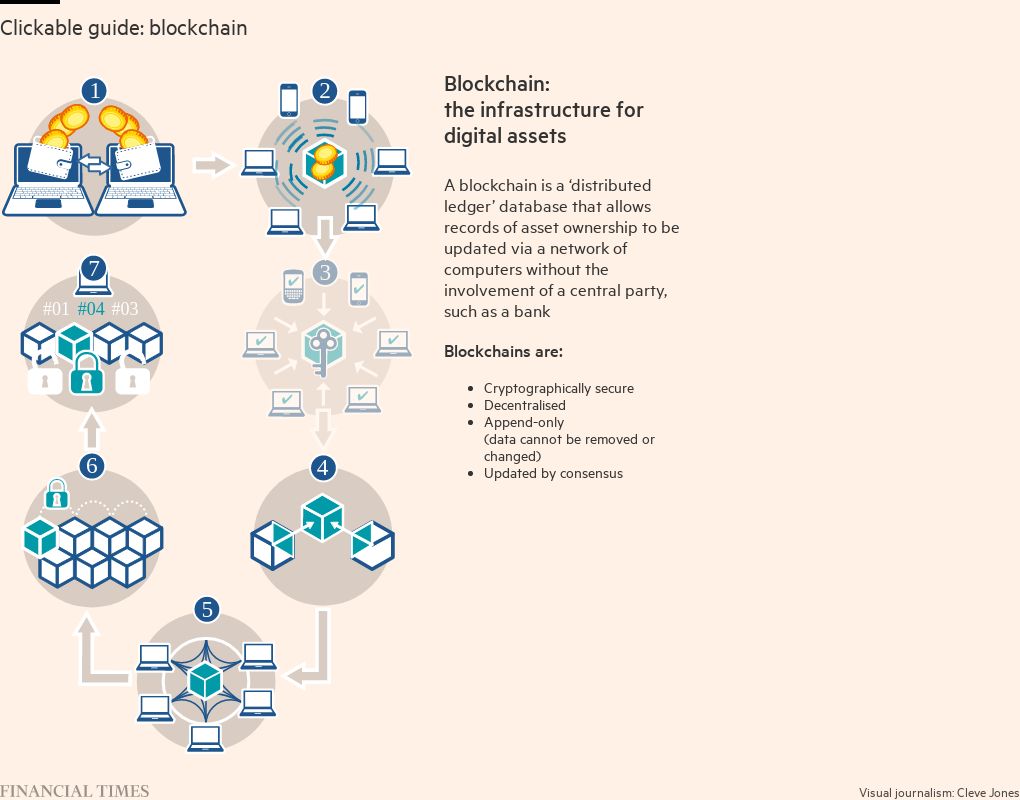

Financial experts, however, say the promise of blockchain technology and its potential to change Wall Street and beyond remains. One of the main reasons for this has to do with what a blockchain is.

Blockchains, often described as distributed ledgers, are inherently sophisticated but open spreadsheets. Imagine a Google Sheet where the editor gives access to anyone in the world. And there is no single blockchain, but each digital asset, currency or token, has its own blockchain.

The only problem – and this is innovation in blockchain technology and where the “crypto” in cryptocurrency comes from – is that the code that runs the spreadsheet is encrypted. So while anyone can look at a blockchain spreadsheet, to edit it (usually to enter a transaction) you need to have the exact code (sometimes called a key) and you need to enter a change that makes sense in the context of the rest of the spreadsheet.

So even though everyone can view blockchains, they are almost impossible to hack. Not that you don’t hear about blockchain or crypto hacks – there are plenty of them. But most hacks involve accessing key codes, which are stored outside the blockchain.

The fact that blockchains make markets more transparent is a significant advantage for the technology, says David Treat, managing director at technology and capital markets consultancy Accenture. “Everyone gets the exact same information at the same time.” According to him, this corresponds to the direction in which financial markets are moving, namely towards “greater access to information in a verifiable way”.

Why haven’t financial markets already migrated to a blockchain?

So, what is delaying the move to blockchain? This is largely a regulatory issue, says Treat. Regulators must ensure that markets are fair and therefore must approve changes. This slows down the speed with which markets can migrate to new infrastructure – especially in securities, such as bonds, commodities or stocks, in which individual investors have already invested significant amounts.

Another obstacle, according to industry experts, concerns liquidity. The most active markets tend to offer the best prices and lowest transaction costs, even if the technology and market structure are better elsewhere. This may be why blockchains have taken off in crypto markets, which were non-existent before this technology, but not, for example, in the bond market, where billions of dollars are already traded via established networks.

Where has blockchain been adopted?

Observers say the most immediate areas of growth in blockchain use are in functions adjacent to trading and spot markets, such as settlement and transaction processing. Connecting transactions recorded on the blockchain to those recorded off a blockchain has been the problem here.

But several companies, the largest of which is Web3 Chainlink services platform, has developed software that connects blockchains to external data. Earlier this year, Swift, the global financial messaging platform jointly owned by the world’s largest banks, announced a partnership with Chainlink. In August, Swift and Chainlink successfully tested a system that could transfer value from one blockchain to another, allowing open, but siled, networks to communicate with each other.

In another sign of the broader adoption of blockchain in traditional banking, Citigroup and JPMorgan have announced blockchain projects in recent weeks.

Citi is testing a blockchain project that will allow its institutional and corporate clients to transform cash into digital tokens, making it easier to transfer money when traditional financial markets are closed. For now, Citi’s tokens can only be moved internally, but the bank is working with regulators and others in the financial industry to create an architecture that will allow tokens to be moved between banks and d other institutions.

In early October, JPMorgan announced that it was beginning to process transactions between clients using a settlement network built with blockchain technology.

“When I step back and look at blockchain projects in traditional financial markets, I think the progress has been pretty good,” says Accenture’s Treat. “The vision of simplified blockchain-enabled networks is here – it just takes time.”